We are characterized by a reliable combination of digital know-how, experienced specialists and renowned partners.

Back

Market update Q2, first half of 2025

The first half of 2025 was marked by Donald Trump's security policy, among other things. The US-Ukraine scandal in the Oval Office on February 28, 2025, had a strong impact on the money market, while the provocative US tariff policy introduced at the beginning of April had little effect.

The crises in the Middle East surrounding Iran, Israel, and Gaza are putting additional pressure on money market rates.

US customs policy leads to risk premiums and discounts

Provocative tariffs introduced at the beginning of April are having a strong impact on returns. Over the course of the second quarter, the premiums will be offset by a moderation in customs policy. The heated geopolitical security situation is leaving the capital market cold.

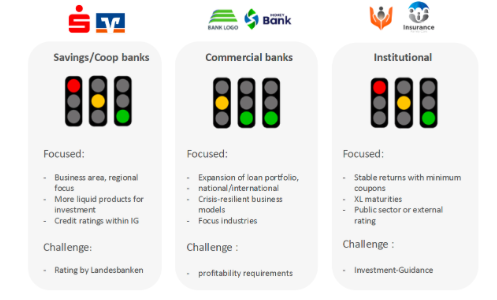

Investor behavior is currently as follows:

▪ Savings banks are currently acting very selectively – their particular interestsand use of investment alternatives are becoming clear.

▪ Commercial banks in Germany and abroad dominate the SSD market. Here, there is increased interest in expanding loan books.

▪ Institutional investors remain relatively unchanged in their interest – here, valuability and security continue to play a major.

Outlook for the second half of 2025:

▪ We expect the strong performance of the second quarter to continue in the second half of the year.

▪ Market volume of around EUR 23 billion expected in 2025 (above the previous year's level).

▪ The need for transformation is increasing financing requirements and calling for a broader investor base.

▪ More pronounced risk/return trade-offs.

▪ Market continues to focus on strong credit ratings (avoidance of defaults).